Effective July 1, 2026, the federal student loan landscape has just experienced its biggest seismic shift in decades through the One Big Beautiful Bill Act (OBBBA). The sweeping OBBBA student loan impacts have completely rewritten the rules for higher education funding, borrowing caps, and repayment options.

If you are a student, parent, or borrower, the system you used to know is officially gone. Here is an exhaustive, comprehensive guide from ScholarshipOwl to help you understand all of the changes, the legal battles currently altering loan caps, and the strategic roadmap to funding your education debt-free.

The Two New Repayment Plans

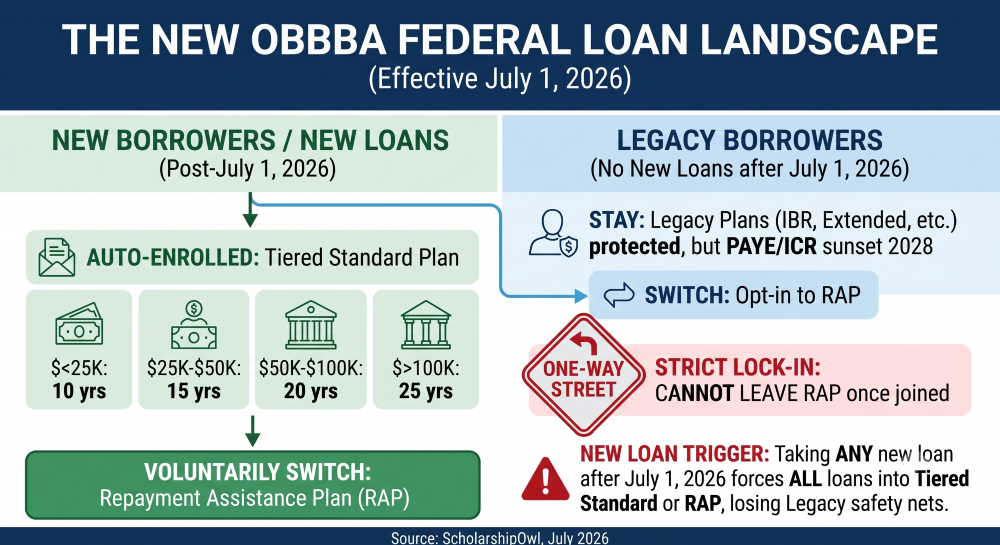

The OBBBA dramatically simplifies the federal repayment system by channeling new borrowers into just two primary tracks: a time-driven plan and a modified income-driven plan.

The Tiered Standard Plan

Unlike the legacy 10-year standard plan, this new plan structures your repayment timeline entirely based on how much total debt you owe:

-

-

- Under $25,000: 10-year term

- $25,000 to $49,999: 15-year term

- $50,000 to $99,999: 20-year term

- $100,000 or more: 25-year term

-

Minimum Payment

Under the Tiered Standard Plan, your monthly payment is calculated mathematically based on your total debt spread out over a fixed timeline (10 to 25 years).

No Access to Eventual Loan Forgiveness

Due to the way that payments are calculated for borrowers in the Tiered Standard Plan, it is not possible to access loan forgiveness. Loan forgiveness is only possible for students on an income-driven repayment plan.

The Repayment Assistance Plan (RAP)

RAP replaces previous income-driven plans, such as the Biden-era SAVE plan, which is being wound down after a long two-year legal pause. RAP is the only income-driven repayment (IDR) plan that is available to new borrowers, or to existing borrowers who take out additional loans on or after July 01, 2026.

Crucial Shift for Minimum Payment Calculation: AGI vs. Discretionary Income

Unlike older plans that calculated payments based on discretionary income, RAP calculates your monthly payment using your Adjusted Gross Income (AGI). This means payments will generally be higher than older IDR options. Knowing your AGI helps you easily predict your progressive 1% to 10% monthly payment under the RAP guidelines.

What is my AGI?

Since the new RAP plan calculates your monthly student loan payment based on your Adjusted Gross Income (AGI), you need to know what this number actually means.

How the IRS Defines Adjusted Gross Income (AGI)

You might know that your gross income is the total money you earn in a year before taxes. Your AGI is that total amount minus a few specific deductions (like retirement contributions). It is the final amount the government is allowed to tax.

Find Your AGI on Your Tax Return

If you have filed taxes, your AGI is a specific line item on your federal tax return. On a standard Form 1040, you will find it clearly labeled on Line 11.

Working But Never Filed a Tax Return?

If you have not filed a tax return yet, that doesn’t mean you’ll have a $0 payment.

Your loan servicer will calculate your minimum payment amount based on a process called “Alternative Documentation of Income”:

-

-

-

-

- You must submit your recent pay stubs (usually the last 30 to 90 days) or an official employer letter showing your gross salary.

- Your loan servicer will project your current earnings into an annual amount and use that as your temporary AGI.

- If your pay stubs show only your gross income and don’t include retirement or healthcare pre-tax deductions as line items, your monthly RAP payment might be slightly higher until you file your first real tax return the following spring.

-

-

-

Income-Driven Minimum Payments

Payments scale progressively from 1% to 10% of your AGI depending on your income bracket. If your AGI is over $100,000, you pay a flat 10% of your AGI. Note that the absolute lowest payment offered is $10; there is no longer a way to get a $0 payment, even if you are unemployed and/or have extreme financial hardship.

Each year, you’ll need to re-certify your income so that your payment can be recast if needed, based on your updated AGI.

No Cap on Monthly Payments

Unlike older IBR plans, there is no monthly payment cap. If your income spikes, your payment spikes—even if it exceeds what you would have paid on a standard 10-year plan.

This is important to understand, because while in early-career roles, your income is likely to be lower. But as you gain experience in your field, you might attain a salary of $100,000 or more. And if you live in a higher cost of living state like California or New York, you might reach that level of salary within just a few years of graduating college. Since there is no cap on your monthly payments, as your salary increases over time, you may find that your student loan payments are as high – or even higher – than your rent or mortgage.

Reduced Minimum Payments with Dependents

For borrowers with dependents, RAP offers something that the Tiered Standard Plan does not – each eligible dependent reduces your monthly payment by $50.

Waived Interest and Matching Payments

RAP features a “no negative amortization” rule—if your calculated payment doesn’t cover the monthly interest, the government waives the rest, as long as you make your minimum payments on time.

Furthermore, if your payment doesn’t reduce your principal balance by at least $50, the government will contribute a matching principal payment to ensure your balance goes down by $50 every month. Note: Making extra payments can actually cancel out the opportunity to receive these subsidies, so sticking to the billed amount is usually best.

Access to Eventual Loan Forgiveness

Your remaining balance, if any, is forgiven after 30 years (360 qualifying payments).

Legacy Plans: Who Can Stay and Who is Forced Out?

The rules regarding whether you can keep an older repayment plan (like IBR, Extended, or the traditional 10-year Standard) depend strictly on when your loans were disbursed.

The “No New Loans” Safe Harbor

If you have federal loans but take out zero new loans on or after July 1, 2026, you are permitted to remain on legacy plans (like IBR). You also have the option to voluntarily opt into RAP.

Note: If you are considering switching to RAP, be sure to read the next section about switching to understand the impact on your “loan forgiveness clock.”

The Hard Trigger

The moment you accept any new Direct Loan disbursed on or after July 1, 2026, you lose access to older plans across all of your loans. Your entire federal balance must transition to either the Tiered Standard Plan or the RAP plan.

The July 01, 2028 Legacy Plan Sunset

For legacy borrowers using older Income-Contingent Repayment (ICR) or Pay As You Earn (PAYE) plans, the OBBBA officially sunsets these programs on July 01, 2028. Servicers will transition remaining users to the new pathways by then.

Repayment Plan Switching: The “One-Way Street” Trap

Can you switch between the Tiered Standard Plan and the new income-driven RAP plan? Yes, but the OBBBA introduces a high-stakes catch.

For New Borrowers (Post-July 2026)

-

-

-

Switching from Standard Tiered Plan to RAP: Allowed. If you start on the Tiered Standard Plan, you can voluntarily opt into RAP at any time.

-

Switching from RAP to Standard Tiered Plan: STRICTLY PROHIBITED. Once you sign up for RAP, you are legally locked in. Because RAP scales up to 10% of your total AGI with no maximum cap, if your career takes off and your income spikes, you cannot escape back to a fixed standard payment timeline.

-

-

For Legacy Borrowers (Pre-July 2026)

If you are an existing borrower, you have the right to voluntarily move from an older plan (like IBR) into RAP. However, protect your progress:

-

-

-

Switching to RAP: If you switch into RAP, your past qualifying payments will transfer over to RAP’s 30-year forgiveness clock.

-

Returning from RAP to a Legacy Plan: If you later leave RAP to return to a legacy plan, your forgiveness clock resets. Months spent paying under RAP do not count toward older legacy plan timelines.

-

Beware of Consolidation: If you consolidate your legacy loans on or after July 1, 2026, your income-driven forgiveness clock immediately resets to absolute zero, and you lose access to all legacy safety nets.

-

-

Impacts on Public Service Loan Forgiveness (PSLF) Program

The Public Service Loan Forgiveness (PSLF) Program is a federal initiative designed to encourage individuals to enter and remain in full-time public service jobs offered through a government or non-profit organization. For borrowers who meet the criteria to access forgiveness through PSLF, the federal government will completely forgive the remaining balance on your Direct Loans, tax-free. To earn forgiveness, you must fulfill all three of the following requirements:

-

-

-

-

Make 120 on-time, monthly payments (equal to 10 years).

-

Be enrolled in a qualifying repayment plan (like the new RAP plan or a legacy income-driven repayment plan).

-

Maintain certified, full-time employment with an eligible public service employer while making those payments.

-

-

-

Public Service Loan Forgiveness remains safe for borrowers who are working for eligible employers, AND who are enrolled in a qualifying repayment plan.

Win more scholarships with less effort

Simplify and focus your application process with the one-stop platform for vetted scholarships.

Check for scholarshipsWhich Plans Are Eligible for PSLF?

Here are the only plans that are eligible for participation in the PSLF Program:

The Repayment Assistance Plan (RAP)

If you take out any new loans on or after July 1, 2026, this is your only income-driven option that would make it possible to access the PSLF Program. Every on-time, full monthly payment you make under RAP while working for a qualifying public service employer counts toward your 120 payments.

PSLF-Eligible Legacy Plans

If you are a legacy borrower who has not taken out any new federal student loans after July 1, 2026, you can continue to use older income-driven plans to rack up PSLF credits:

-

-

-

-

Income-Based Repayment (IBR): This plan remains open indefinitely to legacy borrowers and is often preferred if a borrower has a non-traditional family size (since it handles dependents more broadly than RAP).

-

Pay As You Earn (PAYE): Fully eligible for PSLF, but it stops accepting new enrollments and will be permanently sunset by July 01, 2028.

-

Income-Contingent Repayment (ICR): Fully eligible for PSLF, but like PAYE, it also stops accepting new enrollments and will be completely retired by July 01, 2028.

-

SAVE / REPAYE: These plans are closed to new enrollments and are being actively phased out. Past months spent on these tracks count toward your 120-payment goal.

-

-

-

Switching Plans While in PSLF

Switching between RAP and eligible legacy plans will not wipe out your 10-year PSLF progress, provided you maintain qualifying employment.

The End of $0 Hardship Pauses: New Restrictions on Deferment and Forbearance

Historically, if you fell on hard times, lost your job, or faced severe financial hardship, the federal government provided an easy safety net. You could pause your student loans using an Unemployment Deferment, an Economic Hardship Deferment, or a general servicer forbearance, dropping your required monthly payment to $0.

Under the OBBBA, that system is being fundamentally re-engineered—but how it impacts you depends strictly on the date your loans were born.

For New Loans (Disbursed On/After July 01, 2027)

If you take out new federal student debt on or after July 1, 2027, the traditional safety net is gone:

Elimination of Deferments

The Economic Hardship Deferment and Unemployment Deferment are entirely eliminated for new loans.

The New Forbearance Ceiling

General loan forbearance has been slashed. Instead of being able to request 12 months at a time for up to a cumulative 3-year maximum, new loans are restricted to a hard cap of 9 months of total forbearance within any 2-year period.

The RAP Hard Floor

If you use the new income-driven RAP plan, the system forces a progressive bracket with a hard minimum floor payment of $10 per month. Even if your income drops to absolute zero, a RAP statement will never generate a $0 bill.

For Legacy Loans (Disbursed On/Before June 30, 2027)

There is a massive safe harbor here for existing borrowers. If your federal loans were first disbursed on or before June 30, 2027, you are legally grandfathered into your original terms:

Retain Full Access:

Borrowers with legacy loans who don’t take out ADDITIONAL loans on or after July 01, 2026:

-

-

-

-

- You retain full access to traditional Unemployment and Economic Hardship Deferments.

- You can still access a $0 payment via legacy plans or a standard 12-month forbearance if you face a financial emergency.

- These older safety nets remain legally active for you until every single one of your pre-2027 loans is paid in full.

-

-

-

What Happens After My Legacy Plans Sunset on July 01, 2028?

Letting your old loans hit the 2028 Sunset forces you into one of the two new repayment plans (Tiered Standard Plan or RAP), but preserves your underlying legal right to use old-school $0 hardship pauses if you hit an emergency, because your loans were originated before the 2027 expiration date.

Exception

If you are enrolled in a legacy plan and want to take out a NEW student loan on or after July 01, 2026, then ALL of your loans must transition to either the Tiered Standard Plan or the RAP Plan, and these borrowers will lose their legacy protections, locking you into the strict new system for all of your debt.

The Takeaway

The OBBBA cuts off the $0 pause safety net for the future generation of borrowers, forcing a minimum financial engagement ($10 on RAP) or tightly restricting payment freezes.

However, if you are a legacy borrower who keeps their old loans intact and avoids taking out new debt past the 2027 deadline, your ability to pause your payments at $0 during a financial crisis remains completely protected.

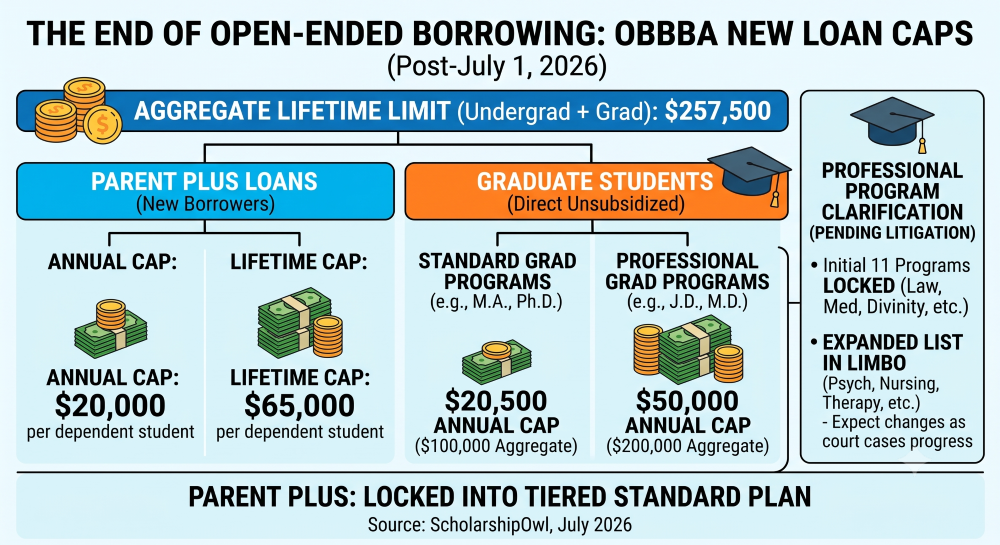

The Graduate Loan Cap Crisis: “Professional” vs. “Standard” Programs

The era of open-ended federal borrowing is over. The OBBBA caps lifetime federal student loan borrowing across all levels of study (undergraduate + graduate) at a hard ceiling of $257,500. Furthermore, Graduate PLUS Loans have been entirely eliminated for new borrowers as of July 01, 2026.

Graduate students must now rely solely on Direct Unsubsidized Loans which are strictly split into a two-tier system:

Standard Graduate Programs

Capped at $20,500 annually ($100,000 aggregate lifetime limit).

Professional Graduate Programs

Eligible for up to $50,000 annually ($200,000 aggregate lifetime limit).

The Initial 11 “Professional” Programs

The Department of Education’s final rulemaking originally restricted the higher $50,000/year “professional” tier to just 11 specific degree fields:

-

-

-

-

- Law (J.D. or LL.B.)

- Medicine (M.D.)

- Osteopathic Medicine (D.O.)

- Dentistry (D.D.S. or D.M.D.)

- Veterinary Medicine (D.V.M.)

- Pharmacy (Pharm.D.)

- Optometry (O.D.)

- Podiatry (D.P.M., D.P., or Pod.D.)

- Chiropractic (D.C. or D.C.M.)

- Theology/Divinity (M.Div. or M.H.L.)

- Clinical Psychology (Ph.D./Psy.D. — added during negotiations)

-

-

-

Legal Challenges & Proposed “Expanded List”

Just days before the July 01, 2026 effective date, a major federal court decision resulted in a temporary stay blocking the Department of Education from using its newly narrowed, restrictive definition of a “professional program.” The court ruled that the Department couldn’t arbitrarily shut out other fields that historically met professional standards.

Because the narrow definition is on hold, the Department of Education has been forced to put forward a pending, “expanded list” of additional qualifying programs that may temporarily access the higher $50,000 cap while litigation plays out. This expanded list includes the following degree programs:

-

-

-

-

- Rabbinical Studies (M.H.L.)

- Counseling Psychology (Psy.D.)

- School Psychology (Psy.D.)

- Clinical Child Psychology (Psy.D.)

- Health/Medical Psychology (Psy.D.)

- Family Psychology (Psy.D.)

- Forensic Psychology (Psy.D.)

- Clinical, Counseling and Applied Psychology, Other (Psy.D.)

- Audiology/Audiologist (AuD)

- Speech-Language Pathology/Pathologist (SLP)

- Anesthesiologist Assistant (CAA)

- Physician Associate/Assistant (MSPA; PA)

- Athletic Training/Trainer (MSAT; MAT)

- Occupational Therapy/Therapist (OT; MSOT; OTD)

- Physical Therapy/Therapist (PT; DPT)

- Registered Nursing/Registered Nurse (MSN)

- Nurse Anesthetist (DNAP)

- Nursing Practice (DNP)

-

-

-

Current Status

Everything is in limbo. While the initial 11 programs are 100% locked into the higher tier, the expanded list is still pending final implementation guidance as colleges scramble to adjust financial aid packages.

In addition, an entirely separate lawsuit has been brought by a coalition of states and Washington D.C., challenging the Department’s emergency implementation. Expect further adjustments as these court cases progress.

The Grandfather Clause

If you were already enrolled in a graduate program and borrowed a Direct Loan or Grad PLUS loan before July 01, 2026, you are temporarily safe. You are grandfathered into the legacy higher limits to complete your current program for up to three academic years (or until graduation, whichever comes first).

Impacts on Parent PLUS Loans

A Parent PLUS Loan is a federal student loan that biological or adoptive parents (and in some cases, stepparents) can take out to help pay for their dependent child’s undergraduate education.

Unlike standard federal student loans for undergraduate students, Parent PLUS loans require a credit check to ensure the borrower does not have an adverse credit history. Additionally, the parent is legally responsible for paying back the loan—the debt cannot be transferred into the child’s name.

Strict New Loan Caps on Parent PLUS Loans

Historically, Parent PLUS loans allowed parents to borrow up to the total Cost of Attendance (COA) of a university. Under the OBBBA, new Parent PLUS borrowers face stringent strict limits:

-

-

-

Annual Cap: $20,000 per dependent student.

-

Lifetime Cap: $65,000 per dependent student.

-

-

(Note: This limit applies per student, not per parent. If both parents borrow for one child, their combined limit is still $20,000/year).

Repayment Plans for Parent PLUS Loans

New Parent PLUS Loans Disbursed On or After July 01, 2026

Borrowers of Parent PLUS Loans disbursed on or after July 01, 2026 are restricted exclusively to the Tiered Standard Plan and are locked out of RAP.

Legacy Parent PLUS Loan Rules

-

-

-

-

- If a parent borrowed a PLUS loan for a student prior to July 01, 2026, or if the student held a Direct Loan for that program before that date, they can continue to borrow up to the full cost of attendance for up to three years, provided the student stays continuously enrolled at that institution in that exact program.

- Legacy Parent PLUS Loans taken out prior to July 01, 2026 to support the same dependent student as a NEW Parent PLUS Loan will also be forced to move to the Tiered Standard Plan. Legacy Parent PLUS Loans taken out prior to July 01, 2026 that support a different dependent student can remain with their existing legacy loan.

-

-

-

Access to PSLF for Parent PLUS Loans

Because new Parent PLUS loans disbursed on or after July 01, 2026 are restricted exclusively to the Tiered Standard Plan and locked out of RAP, new Parent PLUS borrowers have no pathway to PSLF.

If a borrower is pursuing PSLF, they must ensure they are on either RAP (for new and switching borrowers) or IBR (for legacy borrowers). Leaving your loans on the default Tiered Standard Plan will completely halt your progress toward tax-free public service forgiveness.

Which OBBBA Repayment Plan is Right for You? A Self-Assessment Checklist

Because the OBBBA turns the Repayment Assistance Plan (RAP) into a permanent, one-way street, choosing your repayment plan is no longer a decision you can make carelessly. Once you choose RAP, you cannot switch back to the Standard Tiered Plan.

To determine the best path for your unique situation, sit down with a calculator and ask yourself these foundational questions:

1. What is your career trajectory and income potential?

Consider the Tiered Standard Plan:

If you expect your income to grow rapidly or you are entering a high-paying field, this may be a better plan for you. Because the Standard plan is locked into a predictable, fixed mathematical payment based strictly on what you owe, a skyrocketing salary won’t increase your monthly bill.

Consider the RAP Plan

If you are entering a career field with lower or highly variable starting wages, you might want to choose the RAP Plan. Because it scales progressively from 1% to 10% of your AGI, it provides an immediate shield against high monthly bills while your income is low.

2. Are you tracking toward Public Service Loan Forgiveness (PSLF)?

-

-

-

- If YES, your choice is essentially made for you. The default Tiered Standard Plan does not count for PSLF credit. To earn tax-free government forgiveness after 10 years, new borrowers must opt into RAP.

- If NO, you can freely weigh both options based purely on out-of-pocket costs and interest accumulation.

-

-

3. Do you prioritize minimizing overall interest or lowering monthly bills?

Pay the Least Amount of Interest

If your goal is to pay the least amount of total interest over the life of the loan, the Tiered Standard Plan forces you to aggressively chip away at the principal on a strict 10-to-25-year countdown, getting you out of debt faster.

Maximize Short-Term Cash Flow

If your goal is maximizing short-term cash flow, the RAP Plan prioritizes monthly affordability. Your monthly payment will not be more than 10% of your income, offers a $50 monthly credit per dependent, and waives negative amortization interest. However, remember that RAP can last up to 30 years, meaning you may pay more in total interest over time if your balance isn’t forgiven. And since there is no cap on your minimum payment, your monthly payments could grow higher than you anticipate as your earnings increase over time.

4. How do you feel about predictability and rules?

Consider the Tiered Standard Plan

If you want predictable stability, you may prefer the Tiered Standard Plan. Your payment remains the same every single month until the balance hits zero, and you can pay the loan off early at any time without penalty or loss of subsidy. But remember that you can’t access forgiveness through the PSLF Program with this plan.

Consider the RAP Plan

If you are comfortable with strict boundaries and prefer initial lower payments, you may prefer the RAP Plan. You must legally recertify your income every single year, and your payment will automatically rise if your income rises (with no maximum cap). You also will need to accept that you can never leave the plan once you are enrolled.

5. For Legacy Borrowers Only: Should you stay on a legacy plan or switch to the new RAP Plan?

If you are a legacy borrower (all loans taken out before July 1, 2026) and you are done borrowing, you have a unique advantage: you get to decide whether to stick with your current plan or voluntarily switch to the new system. To find your best path, consider these four factors:

Your Income Outlook (IBR vs. RAP)

Keep legacy Income-Based Repayment (IBR) if you expect your salary to skyrocket. IBR has a built-in safety valve—your payment can never exceed the original 10-year Standard amount. RAP has no upper limit; if your income spikes, your monthly bill will rise with it.

The Cost of Safety Nets

Stick with a legacy plan if you rely on a $0 monthly payment during financial hardship. Older tracks allow a true $0 bill, whereas RAP enforces a mandatory $10 per month floor even if your income hits absolute zero.

The Dependent Credit

Consider switching to RAP if you have multiple children. RAP deducts $50 per month from your payment for every dependent in your household (down to that $10 minimum), a feature older legacy plans do not match.

The 2028 Sunset Deadline

If you are currently on PAYE or ICR, your plan will completely sunset on July 01, 2028. You don’t need to panic today, but you should use the StudentAid.gov Loan Simulator to compare whether moving to Legacy IBR or the new RAP plan makes the most sense before your servicer automatically transitions you.

The Golden Rule: Do Not Consolidate Your Loans

If you decide to switch, change your repayment plan directly. Do not consolidate your loans.

Consolidating legacy loans after July 01, 2026, acts as a legal reset button—it will instantly vaporize your past forgiveness progress and permanently strip away your grandfathered $0 hardship protections!

Next Step: Run Your Numbers

Do not guess. Head over to StudentAid.gov and use the official Loan Simulator tool. Plug in your current total debt, your expected starting salary, and your household size. Compare the Total Amount Paid and the Monthly Payment under both tracks to see the exact mathematical difference before you officially sign on the dotted line.

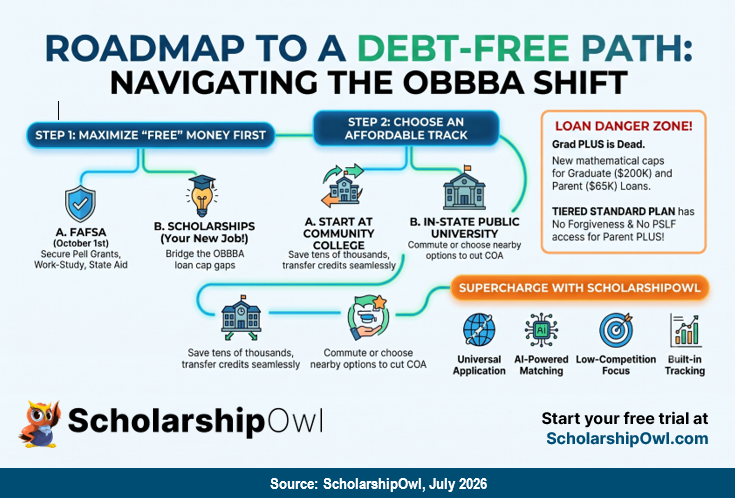

The Ultimate Pivot: Prioritizing a Debt-Free Path

With federal loan caps dropping and Grad PLUS dead, relying on Uncle Sam to bankroll 100% of your higher education is no longer a viable strategy. Now more than ever, students must prioritize an affordable, debt-free path to college.

Step 1: Max Out “Free” Money First

Before even looking at a loan application, exhaust every single source of funding that you don’t have to pay back:

The FAFSA

Complete the Free Application for Federal Student Aid (FAFSA) early to claim federal entitlements like the Pell Grant, work-study programs, and state-specific grants. The FAFSA opens on October 1st every year. Apply at www.fafsa.gov.

Scholarships

Treat applying for scholarships like a part-time job. Every dollar earned through scholarships helps to bridge the gap created by the OBBBA’s new loan ceilings.

Income & Family Support

Lean into part-time employment, paid co-ops, and intentional family contributions to chip away at education costs in real-time.

Step 2: Choose the Most Affordable Path to College

Do not buy a Ferrari when a reliable sedan will get you to the same destination.

Get Started at a Community College

Starting your education at a community college to complete your general education requirements is one of the smartest financial moves you can make. You can save tens of thousands of dollars, completely avoid early student debt, and seamlessly transfer those credits to a four-year public university to finish your degree.

Consider Online Programs

Earning college credits online enables you to fit your classes in around your job and family responsibilities. It also lets you continue living with your family rather than moving out to live on a college campus, which significantly reduces the cost of your education. Best bet for online programs: Enroll in online classes offered by a community college in your state. Then when you are ready to transfer, you can transfer your online community college credits to a university, just as if you completed the classes in-person.

Choose a University Near Home

When you are ready to transfer to a university, or if you prefer to enroll at a university for all four years of college, focus on colleges that are near your home. You may be able to avoid the cost of living on campus and commute from home instead. Even if you don’t live close enough to the college to be able to live at home, it’s better to choose an in-state public university than a private college or out-of-state college in most cases.

Avoid Enrolling in Private Trade Schools

The majority of programs that are available at a private trade school are ALSO available at a community college. Community college tuition is very affordable; private trade school tuition is much higher.

Supercharging Your Strategy with ScholarshipOwl

Because the OBBBA makes securing private scholarships an absolute necessity rather than a luxury, having the right tool to manage your search is critical. ScholarshipOwl is designed to take the friction out of the process, moving students away from tedious application forms and into a streamlined, high-efficiency ecosystem.

Key features that give you a competitive advantage include:

Universal Application

Your student profile acts as a universal application for all matching scholarships on the platform. You fill out your details once, eliminating the need to complete repetitive, exhausting application forms.

AI-Powered Recommendations & Matching

The platform uses advanced AI to send you three scholarship recommendations right to your dashboard every week. Over time, the more you apply to scholarships with the platform, the more relevant your recommendations will be.

In addition to your weekly recommendations, you’ll find tons of other matches tailored to your background, field of study, career goals and more.

Focus on Low-Competition Scholarships

Only ScholarshipOwl lets you see the exact number of applicants for each scholarship. This allows you to strategically target low-competition awards where your odds of winning are significantly higher.

Credibility Scoring System

To protect you from scams and marketing traps, the platform features a vetting system that scores the credibility of each scholarship provider, enabling you to prioritize safe, legitimate opportunities.

Built-In Application Tracking

Forget building a spreadsheet to track your submissions. The platform features an integrated dashboard that monitors and tracks the real-time status of your applications.

AI Essay Assistant

Staring at a blank page is the hardest part of writing an essay. Our AI Essay Assistant helps you get started on writing your initial essay drafts, personalized to your background, profile, and responses to questions that you can customize.

Innovative Application Pathways

ScholarshipOwl meets you wherever you are. You can find and apply for scholarships via their new mobile app, a dedicated ChatGPT app, or in some cases, simply by replying directly to a notification email. (And in the near future, you’ll even be able to apply to some scholarships via SMS!)

Opt-In for Automatic Applications & Re-applications

You can opt-in to be automatically entered into all “no requirement” scholarships in your match list. You can even can opt-in to be automatically reapplied to recurring scholarships that select multiple winners year-round, ensuring you never miss a deadline!

The Bottom Line

The OBBBA is forcing a cultural shift in how America pays for college. If you are a student loan borrower, or plan to be, it’s imperative that you understand all of the impacts of the OBBBA. But your best course of action if you are not yet burdened by student debt is to avoid it in the first place. By combining smart institutional choices—like community college tracks—with tech-driven funding platforms like ScholarshipOwl, you can bypass the chaotic new federal loan system entirely and graduate with your financial future intact.

Not yet a member of ScholarshipOwl? Start your free 7-day trial today!

For Further Reading

- Managing Student Loan Debt: The Ultimate Guide for Graduating Students

- When “Yes” Costs Too Much: Smart Strategies for Paying for College

- How to Find and Apply for Scholarships That Are Truly Worth Your Effort

- Scholarship Strategies that Put You on an Affordable Path to College

- Family Can’t Help Pay for College? No Problem: Your DIY Guide to Paying for College on Your Own